Q4 Market Review:

The fourth quarter began with the stock market in a correction. By the close of October, the S&P 500 had experienced a 10.6% decline from its peak in July. Although the S&P 500 maintained a year-to-date increase of over 10%, the S&P 500 equal-weight and the small-cap Russell 2000 were down by 2.5% and 4.6%, respectively. The primary catalyst for this stock market weakness was the sharp increase in interest rates. Over this period, the U.S. 10-year Treasury bond yield surged from 3.81% to 4.99%, reaching its highest level since 2007. Investors expressed concern over the Federal Reserve's aggressive tightening policy and uncertainties surrounding funding the nearly $2 trillion budget deficit.

While there was little change in the fundamentals, several catalysts in November and December led to an epic rally in the financial markets -- the 10-year Treasury bond yield fell by 1.2%, and the S&P 500 rallied by 13.7% during November and December. The U.S. 10-year Treasury bond yield rose to a sixteen-year high in October because investors were concerned that the supply of bonds needed to fund the massive budget deficit would overwhelm demand. On October 30th, the U.S. Treasury Department issued its Quarterly Funding Announcement, which outlines the amount of bonds and bills the Treasury will issue in the next quarter. Typically, the Treasury funds the deficit by issuing 80% bonds and 20% bills that mature in less than a year. On October 30th, the Treasury announced that bonds would account for only 40% of its quarterly issuance. This significant and unexpected reduction in the supply of bonds led to a sharp drop in long-term yields and stoked a massive equity rally.

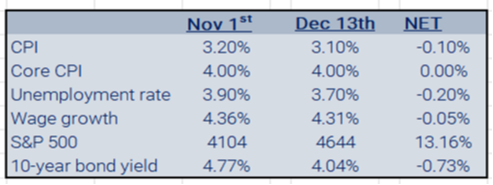

In December, the stock market rally continued because the Fed indicated that it was finished increasing interest rates and was discussing cutting interest rates. The Fed's pivot was unexpected because only two weeks prior, on December 1st, Powell said, "It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance or to speculate on when the policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so." Also, there was no discernable change in the data:

Source: FRED and Barchart

Despite a deeply inverted yield curve, a regional bank crisis, and 20 consecutive monthly declines in Conference Board's Leading Economic Index, the S&P 500 increased by 24.2% in 2023. Since it lost 19.4% in 2022, the S&P 500's 2-year gain was only 0.10%. Additionally, since earnings grew at only 3.3% on a twelve-month trailing basis, the S&P 500's 2023 advance was mainly due to an increase in valuations, which is surprising during a period of rising interest rates.

Source: FRED and Barchart

The S&P 500 valuation increased because most of the index's return was driven by the expensive mega-cap technology stocks. In fact, 62.2% of the S&P 500's return was due to seven names – "The Magnificent Seven" (Apple, Microsoft, Google, Amazon, Meta, Tesla, and Nvida) – which had an average gain of 104.7% in 2023 after an average loss of 45.3% in 2022.

Market Outlook

We rely on the leading economic indicators and the credit-sensitive sectors of the economy to indicate the likely path of the economy so we can position the portfolio to perform well in all economic environments.

The inverted yield curve, the negative money supply growth, the Leading Economic Indicator Index decline, and the contraction in the housing, manufacturing, and durable goods industries indicated that inflation would fall and a mild recession was likely. We positioned the portfolio in defensive sectors of the economy (staples, healthcare, and utilities), built a three-year bond ladder that "locked-in" approximately a 5% yield, and invested in short-term credit.

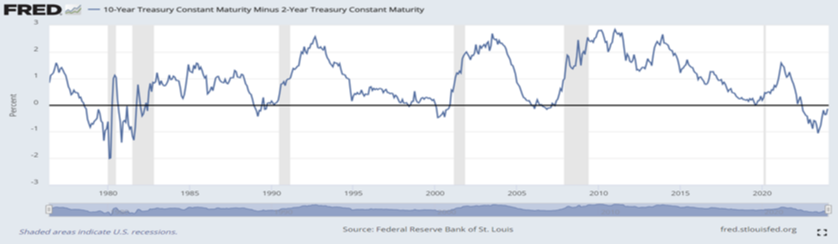

Since 1968, every time short-term rates yielded more than long-term rates, a recession occurred with an average lead time of 14 months. One of the key explanations behind an inverted yield curve's ability to forecast the last eight recessions lies in the challenges it creates for banks and financial institutions, resulting in reduced lending, which leads to slower economic growth. A flattening yield curve after inversion indicates that the recession is imminent.

Source: FRED

In addition to the yield curve, another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959. Historically, when the LEI is below 0 and falling, the S&P 500 has an average return of (11.2%).

Source: Conference Board, Wolfe Trahan & Co.

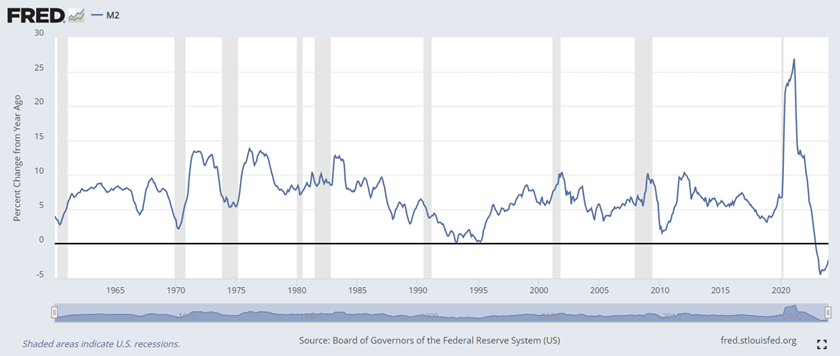

Milton Freidman famously said:" inflation is always and everywhere a monetary phenomenon." The Fed ignored the surging money supply, and inflation rose to a 40-year high. Today, the money supply's growth rate has collapsed, and economic growth and inflation will continue to decline.

Source: FRED

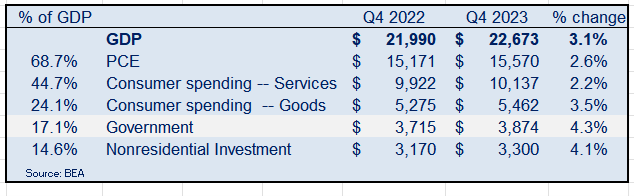

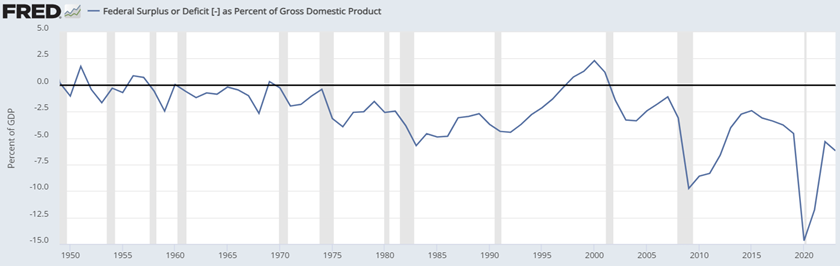

Despite these negative economic indicators, sharply higher interest rates, and a regional banking crisis that produced three of the country's largest four bank failures, the economic slowdown/recession that we positioned for didn't materialize. In fact, this week, the Bureau of Economic Analysis reported that the economy grew at 3.1% in 2023. Unfortunately, much of this growth was due to government spending and a budget deficit that was 6.3% of GDP – a record for a peacetime economy not in recession.

According to the Bureau of Labor Statistics (BLS), 2.7 million jobs were generated in 2023, marking a decrease from the 4.8 million recorded in 2022. Notably, 672,000 of these new positions constituted government jobs, accounting for 24.9% of the total.

In 2023, the federal government's budget deficit was $1.7 trillion, which was a 23% increase from 2022's deficit. The deficit increased from 5.4% to 6.3% of GDP. According to Gavekal Research, the U.S. budget deficit is larger than the S&P 500's profits.

Source: Gavekal

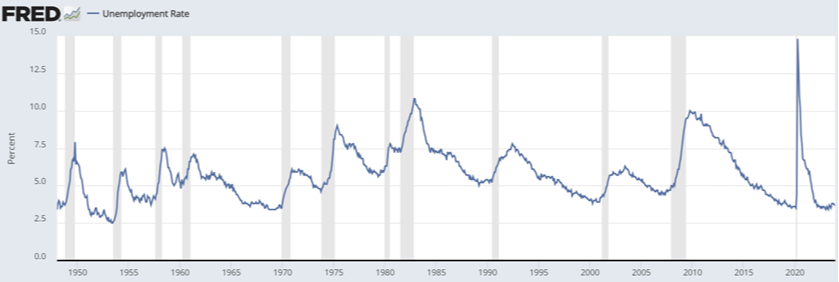

Governments run large budget deficits during wartime or recession. The unemployment rate is near a fifty-year low, yet the budget deficit as a percent of GDP is greater than any post-WWII recession other than the Great Repression of 2008 and the Pandemic.

Source: FRED

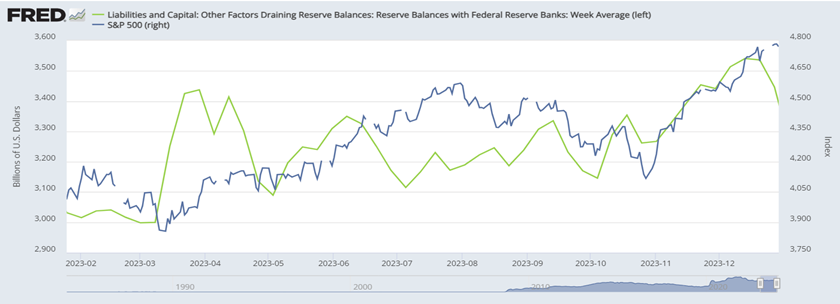

In addition to the government's unprecedented budget deficit, we believe the economy avoided recession in 2023 because significant liquidity was added to the financial system after the banking crisis in the spring and during the fourth quarter. In both periods, the surge in bank reserves led to a significant stock market rally.

Source: FRED

We believe an unprecedented budget deficit and surging liquidity prevented the recession and led to a speculative market environment. Unfortunately, these policies just "kick the can down the road" because our national debt burden surged to pay for this spending.

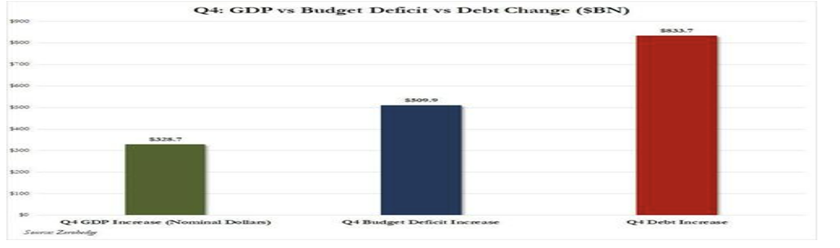

GDP rose by $329 billion in the fourth quarter. In comparison, the budget deficit increased by $510 billion (a 50% increase year-over-year), and the public national debt increased by $834 billion. According to Zerohedge, based on these Q4 numbers, it now takes $1.55 in budget deficit to generate $1 of GDP growth and $2.50 of new national debt to generate $1 of GDP growth. The federal government has mortgaged our future, and now the nation's interest expense is approaching $1 trillion per annum, which is 12% greater than our defense budget.

Source: Zerohedge

In Sum:

In 2023, government spending surged while the Fed aggressively raised interest rates to slow the economy and fight inflation. The economy avoided recession because of the government's massive budget deficit. In December, the Fed claimed victory -- it believed that inflation was subdued without an increase in the unemployment rate – and announced that rate increases were finished and it was discussing cutting interest rates.

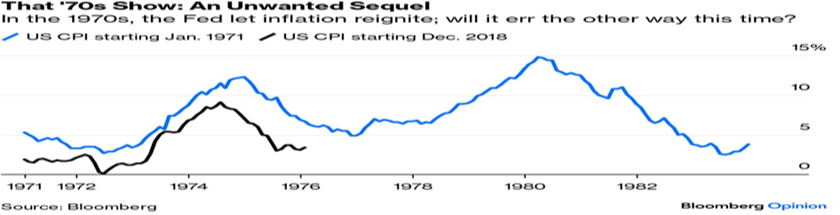

We believe that the Fed's pivot needlessly increases economic uncertainty. Pivoting to a dovish stance while the core CPI is 3.9%, the unemployment rate is 3.7%, and the government is running a massive deficit, increasing the probability that inflation will remain sticky around 3% or accelerate in the future. The Fed pivoted too early in the 1970s, and inflation accelerated until short-term interest rates were increased to 21%, and a deep recession ensued.

Source: Bloomberg

In 2024, we expect that the inverted yield curve, higher interest rates, and increased lending standards will continue to push the economy toward recession. These deflationary drivers will be offset by the government's election-year deficit spending, the loose financial conditions created by the UST manipulation of the quarterly refunding, and the Fed's dovish pivot. While an acceleration in growth is unlikely, we wouldn't be surprised if inflation remains sticky around 3% or increases due to higher oil prices or new supply chain issues. Our base case is deflation (slower growth and declining inflation), yet a stagflationary environment (slower growth, rising inflation) wouldn't surprise us.

Financial Market Outlook

Given the Fed's pivot and the S&P 500's 11.7% Q4 rally, investors are ebullient and believe that the Fed has executed the rare "soft-landing." Investors expect the Fed to cut interest rates six times this year beginning at its March meeting, while S&P 500 earnings are estimated to grow at a robust 13.1%. We believe six rate cuts and 13% earnings growth are mutually exclusive, and since stocks are priced for perfection, the Fed's pivot to an easing bias significantly reduces market risk.

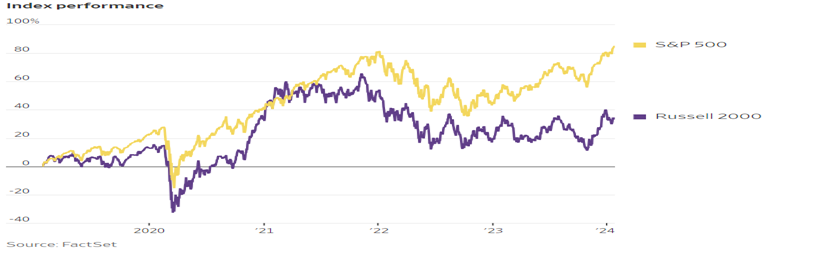

We believe the S&P 500 offers a poor risk-reward because it is overvalued, and seven very expensive mega-cap technology companies make up nearly 30% of the index. While the S&P 500 is at an all-time high for the first time in two years, the technology sector is driving most of that gain. Currently, the other ten sectors of the S&P 500 are, on average, 15% below their record high. Additionally, the Russell 2000 – a broad index of 2000 small-cap companies – remains about 20% below its record November 2021 high.

Source: Wall Street Journal

A narrow market breadth (very few stocks participating in the market rally) indicates that the market is unhealthy and could be vulnerable to a significant correction. This narrow market breadth is consistent with our view of slowing economic growth, not a goldilocks economic environment.

We expect the stock market will trade in a large range with the upside limited by high valuations and the downside protected by the "Fed's Put." After a poor relative year, we expect value stocks to outperform growth, and we will continue to avoid small-cap and low-quality stocks. Given the massive budget deficit, we will continue to favor our short-term bond ladder and avoid long-term bonds.

Portfolio Review:

After a strong relative performance in 2022, our defensive posture led to a disappointing year. We performed well through October but poorly as the financial markets rallied sharply in November and December. While the fundamentals didn't change, we should have adjusted more aggressively to the tacit changes in monetary policy by the U.S. Treasury and the Federal Reserve.

We expect 2024 to be a volatile year, and we believe that stocks will be in a broad trading range with the upside capped by extreme valuation and the downside protected by the "Fed Put." In this environment, we will add to our equity exposure in periods of weakness and reduce our risk exposure when the market is overbought and investors are too optimistic. About 60% of the portfolio is invested in short-duration bonds that yield 5.5%. We think this is a great risk-reward, considering the S&P 500 historical average return is 10% -- i.e., we receive 55% of the market's historic return with limited principal risk.

In Sum

While we are disappointed with our 2023 performance, we are essentially flat over a very volatile two-year period, which is in line with the broader market. We expect this volatility to continue in 2024 since significant economic headwinds remain (slowing growth, elevated core inflation, and rapidly growing debt burden). Despite the economic uncertainty, investors are too optimistic, expecting a "goldilocks" economic environment -- six interest rate cuts by the Fed starting in March while earnings grow at an ambitious 13%. In our view, this outcome is not probable, and we expect volatile corrections as ebullient investors are disappointed.

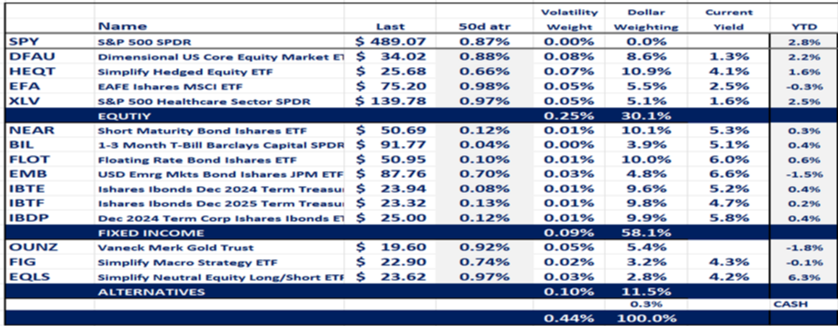

Current Risk-Weighted Model Portfolio:

Our portfolio's risk level (annualized volatility) is 7.0%, which is less than our 60\40 benchmark's risk level of 11.5%.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed.

All investments contain risk.