Stocks have a poor risk-reward and offer a historically low equity risk premium. A 4.9% risk-free rate is great.

Summary

In January, stocks rallied because many investors believed that inflation was defeated and the Fed was poised to reduce interest rates later in the year. Unfortunately, strong February economic data and a reacceleration in the inflation rate indicated that the Fed needed to raise interest rates higher and for longer to combat inflation. Like 2022, nearly all asset classes declined in February as interest rates rose sharply.

While many investors thought the January rally indicated an improvement in the economic outlook, we believed it was a bear market rally. In our view, the rally was driven by favorable seasonality and market flows (corporate buybacks, retirement contributions, speculative positioning, and rebalancing) – not an improvement in the economic outlook.

There is tremendous economic uncertainty. Inflation surged to a 40-year high, and the Fed has aggressively raised interest rates to weaken economic demand and reduce inflation. Unfortunately, the Fed has an almost perfect record – nearly all its tightening cycles lead to recession and an adverse credit event. We believe that a recession is likely this year because the Fed is ignoring the leading indicators of the economy and tightening into an economic slowdown.

Market history shows that the Fed typically raises interest rates until something breaks. This week the Regional Bank Index plunged more than 15% as invested feared that small and mid-sized banks might face a liquidity crisis. Investors became concerned that problems at Silvergate Capital and Silicon Valley Bank (banks that respectively deal with crypto and venture capital customers) may spread to other regional banks. These credit issues are the unintended consequence of the Fed's tightening cycle.

Stocks offer a very poor risk-reward since valuations are at historical highs and corporate profits are in a recession. Sharply higher interest rates drove stocks down last year, and we believe stocks are poised for another decline as the economy slows, and profits disappoint. Bear markets usually trough with the S&P 500 selling less than 14 times peak earnings. Since earnings peaked last March at $210, the S&P 500 could fall to 3000 -- an additional 20% decline.

In this high-risk environment – economic uncertainty, risk of the Ukraine war escalating, and tension with China – we believe a nearly 5% risk-free rate is very attractive. We have a significant investment in a 2-year U.S. Treasury ladder, yielding around 5% and giving us a solid return until the headwinds are reduced, and stocks and bonds offer better risk-reward.

Market Review:

After a solid start to the new year, robust economic data pushed interest rates higher and stocks lower in February. In January, many investors believed that inflation was defeated, and the Fed was poised to reduce interest rates later in the year. Unfortunately, strong February economic data and a reacceleration in the inflation rate indicated that the Fed needed to raise interest rates higher and for longer to combat inflation. Like 2022, nearly all asset classes declined in February as interest rates rose sharply.

Financial Market Performance

The stock market was very strong in January. Many pundits crafted the narrative that the market's strength was because the Fed was successfully orchestrating a soft economic landing, i.e., inflation was receding while the economy was strong enough to avoid recession. The stock market's strong performance and the optimistic narrative created FOMO (fear of missing out) among retail investors who chased stocks higher. According to VandaTrack, retail investors contributed an average of $1.51 billion daily into the stock market in January, the highest amount on record.

We believed that the stock market's strength did not indicate a soft landing -- it was primarily due to seasonal flows into the market and short covering by CTAs and hedge funds. January is usually a strong month for the stock market because of favorable seasonality and large inflows into retirement funds. According to Vanguard, approximately 61% of retirement fund contributions are allocated to Target Date funds that invest in passive ETFs based on your age and not market fundamentals or valuation. Since passive ETFs now control nearly 50% of the stock market, the market is more inelastic, and large flows can significantly impact price.

Since the S&P 500 dropped by 6.1% in December, stocks were oversold, and many trend following strategies (CTAs) and hedge funds had significant short positions. Retirement flows, and target date funds rebalancing pushed stocks higher in January, which led to short covering by hedge funds and CTAs. To make sense of the flows-based rally, many pundits created a soft-landing narrative that fomented FOMO buying among many retail investors. If the stock market rally was discounting a soft landing, that fundamental change should have been reflected in the bond and commodity markets. Instead, as stocks rallied, the yield curve inversion worsened, and the oil declined.

The S&P 500 rallied more than 10% from its mid-December low to its February 2nd high. While many believed that the stock market was signaling a soft-landing, the yield curve and commodity markets didn't confirm this narrative. We believe the market rallied due to passive flows, target fund rebalancing, and short-covering.

Source: Stockcharts.com

In February, stocks and bonds sold off sharply because strong economic data and a rebound in the inflation rate made it clear to investors that the Fed remained behind the curve and had to raise interest rates higher for longer to quell inflation.

We believe that we are in a very high-risk environment with significant uncertainty. Despite a bear market decline last year, the stock market remains overvalued, and earnings expectations seem unrealistic. Additionally, most Fed tightening cycles lead to recession because the Fed primarily focuses on coincident economic indicators to implement monetary policy. The problem is that changes in monetary policy can take 18 months to affect the economy and inflation, so monetary policy is essentially implemented through the rearview mirror. This tightening cycle is more complicated because the pandemic shutdown may have adversely impacted the economic data (especially in the labor market).

Though the labor market is strong, and inflation remains elevated, the leading indicators of the economy – the yield curve, the money supply, LEI, housing permits and starts, and ISM new orders less inventories -- indicate that a recession is likely this summer or early fall.

Market history shows that the Fed typically raises interest rates until something breaks. This week the Regional Bank Index plunged more than 15% as investors feared that some smaller and mid-sized banks might face a liquidity crisis. Investors became concerned that problems at Silvergate Capital and Silicon Valley Bank (banks that respectively deal with crypto and venture capital customers) may spread to other regional banks. These credit issues are the unintended consequence of the Fed's tightening cycle.

Regional banks pay a small yield on customer's deposits and then lend or invest the funds for a higher rate to make a profit. Silicon Valley Bank used its customer's deposits to buy long-term government and mortgage-backed bonds. Recently, depositors pulled their money from the savings accounts, forcing SIVB to sell some of its bond investments at a large loss.

Since many regional banks bought bonds when yields were significantly lower, they have large unrealized losses on their balance sheet. In theory, these losses are only on "paper" because the bank can hold the debt until it matures, and they receive 100% of its principal. The problem is that the Fed lifted short-term interest rates to nearly 5%, and savers are pulling their deposits to earn a higher risk-free yield. As deposits are removed, the bank is forced to sell its investments at a loss, which could lead to a capital shortfall. The contagion risk is that significant losses and capital shortfalls could create fear among savers and lead to bank runs.

The Regional Bank Index plunged 15% this week, as fleeing deposits would lead to large, realized portfolio losses and capital shortfalls. Credit events are typical at the end of a tightening cycle.

In Sum

The overvalued stock market is vulnerable to another decline as the economy slows and corporate profits disappoint. Also, the stock market is at significant risk if there is an escalation in the Ukraine war or if China sends weapons to Russia. While the stock market has a very poor risk-reward, we believe that short-term U.S. Treasuries (two years and less) that yield more than 5% are very attractive. We think it's prudent to "lock in" a 5% risk-free for the next two years until much of the economic and geopolitical uncertainty is resolved.

Economic Outlook:

In February, the Bureau of Labor Statistics reported that 517k jobs were created in January, and the unemployment rate fell to 3.4%, which was the lowest level since 1969. Stocks and bonds sold off sharply because the Fed believes that a strong labor market leads to inflation -- so the good employment news was bad news for stocks.

Inflation surged to a 40-year high because the government and the Fed provided massive monetary and fiscal stimulus to support the economy during the pandemic shutdown. When inflation surged in 2021, the Fed failed to remove its emergency monetary measures because it incorrectly believed that inflation was "transitory." Finally, inflation reached 8.9% last June, and the Fed embarked on its most aggressive tightening cycle in over 40 years.

The Fed believes in the Philips Curve, which is a theory that unemployment and inflation have an inverse correlation – i.e., a low unemployment rate leads to inflation. Accordingly, the Fed must reduce economic demand by increasing unemployment to reduce inflation. The Fed is currently forecasting that it will increase interest rates to 5.25% by December, which will push the unemployment rate to 4.55%, creating a loss of 1.85 million jobs.

In our view, this approach to monetary policy, which creates unemployment to reduce inflation, makes no sense.

First, the theory doesn't always work. In the 1970s, inflation and unemployment were both very high (from 1974 to 1980, the unemployment rate averaged 7.1%, and inflation averaged 8.7%), and in the period between the Great Financial Crisis and the Pandemic, both inflation and unemployment remained low (from 2014 to 2020, the unemployment rate averaged 4.7%, and inflation averaged 1.6%)

Secondly, the Fed uses coincident and lagging data (employment and inflation) to make policy decisions that don't fully impact the economy for at least 18 months. This process of making monetary policy decisions in the rearview mirror is why most tightening cycles lead to a recession and, typically a credit event.

Most Fed tightening cycles led to a recession. Since 1965, every time inflation rose above 5%, a recession occurred.

Source: FRED

Historically, to fight inflation, the Fed tightens until something breaks. This isn't surprising since the Fed focuses on lagging economic indicators (inflation and employment) and ignores the money supply and other leading economic indicators. This week's banking sector problems may be the credit event to mark the top of the cycle.

Source: BofA Research

In addition to using a debunked economic theory to guide monetary policy, the Fed's effort to reduce inflation is being contested by an inflationary fiscal policy. Despite an unemployment rate at a 40-year low and record revenue, the Federal government ran a budget deficit of $1.18 trillion, which is -5.4% of GDP. Budget deficits of this magnitude are inflationary and usually only occur during recession and wartime.

Despite unemployment at a 40-year low and record tax revenue, the budget deficit reached -5.4% of GDP. Budget deficits of this magnitude are inflationary and negatively affect the Fed's effort to reduce inflation.

Source: FRED

Instead of focusing on coincident and lagging economic indicators, the Fed should rely on the economy's leading indicators to guide policy. The yield curve, the Conference Board's LEI, the money supply, and the leading cyclical components of the economy (housing, manufacturing, capital investment) indicated that the Fed was making an inflationary mistake in 2021, and now the indicators are warning that a recession is on the horizon.

The yield curve (ten-year U.S. Treasury bond minus the two-year U.S. Treasury) is the best economic indicator. An inverted yield curve preceded every post-WWII recession. An inverted yield curve indicates economic stress and leads to slower credit growth since most banks/lenders borrow short and long to make a profit. The yield curve is -1.07%, the most inverted since 1981. According to Deutsche Bank's Jim Reid, the yield curve has only been inverted by more than 1.00% four times since 1940 (1969, 1979, 1980, and 1981), and each time a recession was already underway or occurred within eight months.

The yield curve's slope is probably the most accurate economic indicator. Every post-WWII recession was preceded by an inverted yield curve (short-term interest rates yield more than long-term interest rates). The yield curve has been inverted since July and is the most inverted since 1981. Since the yield curve typically inverts 12 months before a recession, a recession will likely occur this summer.

Source: FRED

The housing sector is a critical engine of economic growth. Higher mortgage rates led to a 27% plunge in building permits over the past. A sharp decline in building permits typically presages an economic slowdown or recession.

Source: FRED

While the Fed is concerned that the employment market is too strong, the BLS reported that the number of available construction jobs plunged by 37% over the past year. Since housing is a leading sector of the economy, this weak report may indicate that the labor market is poised to weaken.

Source: FRED

Another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959.

Source: Conference Board

Milton Freidman famously said:" inflation is always and everywhere a monetary phenomenon." Last year, the Fed ignored the surging money supply, and inflation rose to a 40-year high. Today, the money supply's growth rate has collapsed, and economic growth and inflation will likely decline later this year.

Source: Longtermtrends

In Sum

There is tremendous economic uncertainty. Inflation surged to a 40-year high, and the Fed has aggressively raised interest rates to weaken economic demand and reduce inflation. Unfortunately, the Fed has an almost perfect record – nearly all its tightening cycles lead to recession and an adverse credit event. We believe that a recession is likely this year because the Fed is ignoring the leading indicators of the economy and tightening into an economic slowdown. Since a recession is a high probability but not a certainty, we will continue to watch the leading indicators for any signs of improvement.

As an investor, the economy's rate of change is critical to our asset allocation, not whether or not the economy enters a technical recession. Our portfolio is built to perform well in a decelerating growth and falling inflation environment.

Financial Market Outlook:

Despite a bear market last year, stocks are overvalued, corporate profits are falling, and Wall Street analysts' 2023 earnings estimates appear unrealistic. Last year stocks fell because sharply higher interest rates negatively affected stock valuations. This year, we expect another market decline driven by disappointing earnings and lower valuations.

Last year, the S&P 500 fell by 27.5% from its January high to its October low. This first leg of the bear market was driven by sharply higher interest rates that negatively impacted stock valuations. The S&P 500 rallied by 20.1% from its October low to its February 2nd high. While many investors thought this rally indicated an improvement in the economic outlook, we believed this was a bear market. In our view, the rally was driven by favorable seasonality and market flows (corporate buybacks, retirement contributions, speculative positioning, and rebalancing) – not an improvement in the economic outlook.

As discussed previously, market rallies of this magnitude are typical during mid-term election years. In fact, according to BofA Global, since 1930, the S&P 500 rallied 16.6% on average from its mid-term election low through the first half of the following year.

Stocks offer a very poor risk-reward, and we believe the next leg of the bear market has begun. Based on long-term valuation measures (market cap to GDP and Shiller's CAPE), stocks are historically overvalued and vulnerable as profit margins regress to the mean and corporate profits disappoint. Corporate profits typically fall 19% during recessions, and bear markets usually end with the S&P 500 selling at 14 times peak earnings or less (the S&P 500 currently sells at 18.6 times peak earnings).

While pundits forecast a soft landing and Wall Street analysts expect S&P 500 earnings to grow by 11.7% in 2023, corporate profits are already in a recession. According to S&P Global, S&P 500 operating earnings fell by 5.8%, and GAAP earnings fell by 13.1% last year. Slowing economic growth and higher interest rates will adversely impact profit margins (which are near record levels) and lead to declining profits.

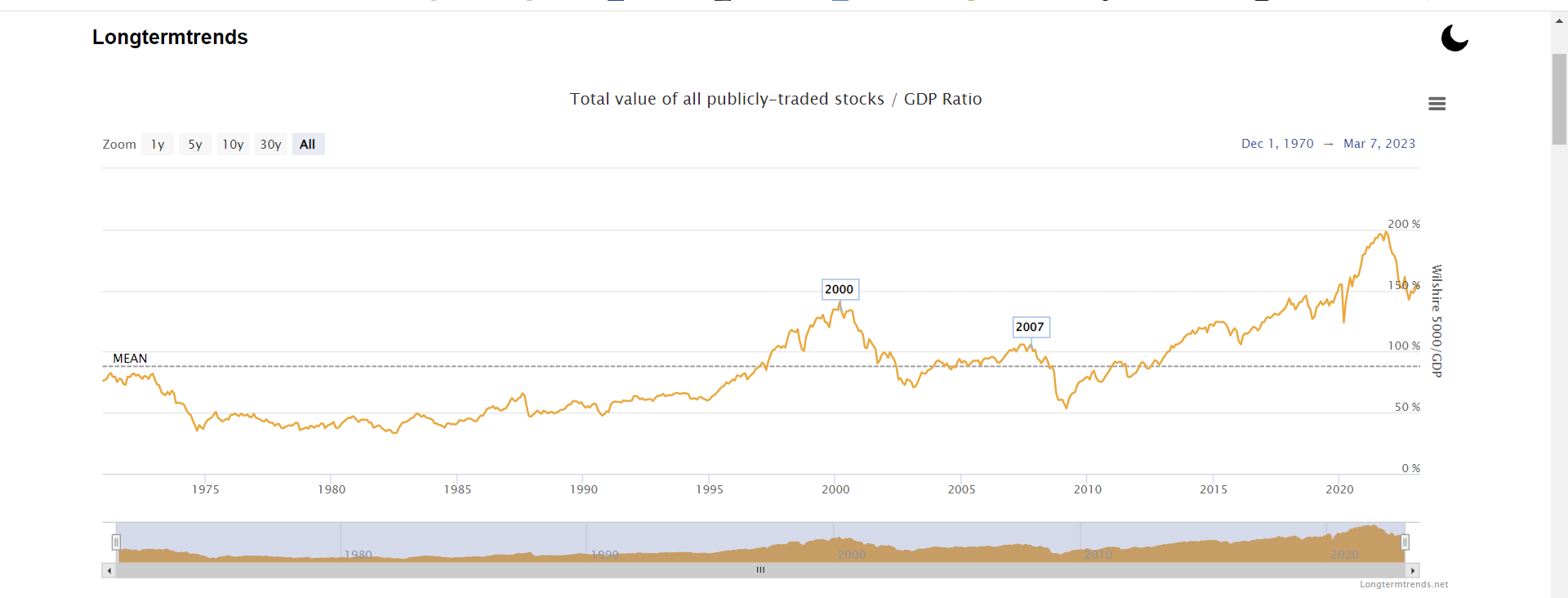

Market Value to GDP -- Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks have never been more expensive.

Source: Longtermtrends

Shiller's CAPE (a valuation measure that smooths out cyclical earnings fluctuations) indicates that stocks are at a historic level of overvaluation despite the vicious bear market last year.

Source: Gurufocus

Corporate profits are 11.1% of GDP, which is about two standard deviations above its 60-year average of 7.2%. Profit margins are highly mean reverting and vulnerable as interest rates rise and growth slows.

Source: FRED

While pundits forecast a soft landing and Wall Street analysts expect S&P 500 earnings to grow by 11.7% in 2023, the GAAP earnings declined 13% last year and are already in a recession. Earnings typically fall 19% during recessions.

Source: Macrotrends

It's not only stocks that are overvalued. Corporate and high-yield debt spreads are below-average levels and indicate investor's complacency. Investors can earn nearly 5% in a risk-free U.S. Treasury bill, yet BAA corporate debt yields only 5.8%, and the S&P 500 has an earnings yield of approximately 5%. Given high stock valuations and low credit spreads, investors are not compensated for taking risk.

The 3-month U.S. Treasury bill is the risk-free rate. Investors are not receiving an adequate risk premium to invest in stocks or corporate bonds. Historically, Baa investment grade bonds yield 4% greater than the 3-month risk-free rate. Despite tremendous economic and geopolitical uncertainty, that spread is less than 1%.

Source: FRED

In Sum:

Stocks offer a very poor risk-reward since valuations are at historical highs and corporate profits are in a recession. Sharply higher interest rates drove stocks down last year, and we believe stocks are poised for another decline as the economy slows, and profits disappoint. Bear markets usually trough with the S&P 500 selling at less than 14 times peak earnings. Since earnings peaked last March at $210, the S&P 500 could fall to 3000, which is an additional 20% decline.

In the high-risk environment – economic uncertainty, risk of the Ukraine war escalating, and tension with China – we believe a nearly 5% risk-free rate is very attractive. We have a significant investment in a 2-year U.S. Treasury ladder, yielding around 5% and giving us a solid return until the headwinds are reduced, and stocks and bonds offer better risk-reward.

Our Model Portfolio:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

Our portfolio is mainly positioned for a recessionary environment – i.e., declining growth rates and falling inflation. We are underweight stocks relative to our 60/40 benchmark and invested in the value stocks and the defensive sectors of the stock market – healthcare, staples, and utilities.

We have significant fixed-income exposure on shorter-term U.S. Treasury notes (two years and less). Short-term Treasuries are attractive because they have a high risk-free yield, which pays us nearly 5% to wait until there is less economic and geopolitical uncertainty.

So far this year, our defensive portfolio has underperformed our benchmark. Investors believed the economy was headed toward a soft landing, and they rotated from the market's defensive sectors to the growth and economically sensitive. Recently, the defensive sectors have performed better as the likelihood of a soft landing faded.

Current Risk-Weighted Model Portfolio:

Our portfolio's risk level (annualized volatility) is 6.7%, which is less than our 60\40 benchmark's risk level of 13.1%.

In Sum:

Significant economic and geopolitical uncertainty exists, and stocks and corporate bonds do not provide an adequate risk premium. We believe we are positioned to perform well in a challenging investing environment. As the economy slows, our defensive equity investments should outperform, and our large 2-year Treasury ladder pays us a solid return to wait for a better environment.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.